Nowadays, most firms have annual budget processes in place. Nevertheless, there are no many of them using a budget process that is fully align with the company strategic execution process. Even many large firms use budgets just as a “merely” finance tool. We have to stress that budget should be an essential tool for turnaround a firm, but in this case budget must be used as a strategic execution tool that really approach, integrate and align all the areas of the company. Let’s review what make a budget a very powerful strategic execution tool.

Annual budget should be an extension of the company strategy

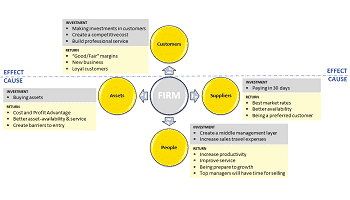

Before presenting the specific company/unit/department budget, a strategy summary (just a few slides) of the company/unit/department should be present. This is the way to guarantee that the budget (short-term planning) is aligned with the strategy (medium and long-term planning). The strategy summary should respond briefly to the following questions regarding growth:

- What is the company positioning compare with competitors?

- What are our differentiators (strategic sweet spots)?

- What is our cost and/or differentiation (competitive advantage)?

- What is the firm strategy (according to the value disciplines, or the core business type framework, etc.)?

- What are our target customer segments (scope)?

- Where is the company expected to be in 2 years, 5 years, and 10 years (vision)?

Budget is not just related with Sales

Unfortunately, there are some top managers that focus budget “just” mainly on sales. They hyper simplify business success just in sales growth. But sustainable and replicable growth required of other functions as solid operations, proper finance structure, etc. Organizations that focus “just” on sales successfully used “to leave a lot of money on the table” because they do not optimize operations. Overestimated operations should affect the capability of the firm to achieve sustainable growth. I mean the growth of the firm is just support for the good performing of the sales, but operations and cost structure are not optimized. Therefore, if sales growth stop or drop the impact in the organization will be huge.

We must have a detailed list of the annual strategic initiatives for each firm/business-unit/department

Budget is not just figures. The figures must be related to coherent initiatives that show the cause and effect relationships between short-term strategy execution and budget. Just if we get in detail at the initiative level and aligning all the company main areas, we can improve strategic execution skills. Moreover, annual budget it is a good moment to: review KPIs; define what the KPIs target for the following year should be; and what resources we need from budget to guarantee success achievements.

Cash flow budget should not be define just for the finance area

There are companies that assume cash flow is mainly an issue for the finance department. However, cash flow is a top strategic decision in which all the areas should participate in the planning process rather than leaving finance to decide what could produce short-term misalignment decisions. The most important cash flow decisions are:

Customers days of payment

It is important to align Sales and Finance in this subject because extending the days of sales outstanding (DSO) is equal to additional customers’ discounts. Furthermore, Sales should define if it is more important extending DSO, or reducing DSO to be able to reduce the days payable outstanding (DPO) what should help us to improve our costs structure to support or sales close process and/or sales profitability.

Supplier days of payment

From the financial point of view, we should extend as much these payments. We must be aware than from the operational and strategic point of view, we could be interested to reduce suppliers days of payment to achieve the following objectives: better cost structure because suppliers will be willing to offer better rates to customers that offer better payment conditions; better services because supplier are willing to prioritize good customers (customers that pay in a shorter period and without delays); better finance conditions because the balance is more solid and banks have less risk; and better days of sales outstanding (DSO) because reducing days payable outstanding (DPO) will push us to improve the DSO.

Inventory days

If Sales, Supply Chain and Finance are not properly aligned about inventory we can face issues like the following: Sales promises services that the firm cannot accomplish for the lack of cash flow, Supply Chain import products according to Sales, and Finance is not prepared to pay importation taxes. The company has to pay for penalties (warehousing costs, etc.) for the delay on taxes’ payments. So the cost structure is suffering, and the brand name is damaged.

Budget alignment example

People and structure must be reviewed

In many companies the people review process leading for Human Resources is not 100% connected with the budget process. Probably because there are still companies that in their understanding budget process is a “pure financial” process rather than a strategic one. Indeed, budget process used to be run between mid-September and late-November, although the people evaluation process used to be run from February to March because the main focus is bonus calculation. So the suggestion is making people review at the same time that the budget process, although final bonus calculation can be calculated next year from February to March. At the same time of the budget process the firm should answer at least the following strategic questions related with people and structure:

- How fast is salaries growing compare with profit growth?

- Do we have the correct productivity?

- Do we have the right balance between direct and indirect staff?

- Should we change our current structure (centralized vs. decentralized, and vertical vs. horizontal)?

- How is each member of the team performing?

- What is the provision for bonuses?

- What is the provision for firing under performers?

- What is the provision for headhunters?

- What is the budget for training?

- What are the MBOs?

Aligning MBOs (Management By Objectives) and bonus program with budget

There are firms that start the new fiscal year and after several months people do not still know what their corporations expect from them. I mean MBOs are not still defined. Even it is worse that people did not participate in the alignment process between budget and MBOs what could create an unmotivated effect in the MBOs because employees can think that MBOs are unfair. On the other hand, we have companies that limit the amount of money that people can obtain via bonus, and they do not use accelerators in the bonus system to motivate high performance behaviors. Those bonus systems that limit the speed of growth could have a “short-term finance justification” but they are strategically unacceptable because it reduces the attractiveness of the firms for top performers, limit employees satisfaction, and reduced the company growth rate.

Monthly and quarterly business and budget review

Well-managed firms used to monthly review the budget and prepare the new forecast for the current fiscal year twice or three times per year. However, many organizations forget to communicate budget and strategy status to the whole company in regular basis (quarterly). If information remain just at the top of the company, we cannot expect the mobilization of the entire company to achieve the budget. So there are firms that pursuing finance confidentiality too much, they reduce the firm speed to get or exceed the budget.

Budget must reflect 100% the most likely scenario

Companies that are in the stock market realize the importance of using the most likely scenario for budgeting. But many firms fall upon temptation to push management to overestimated budget thinking that difficult objectives motivate to work harder and make happier the shareholders. Nevertheless, overestimated budget is a very dangerous decision. Overestimated budget can bring the following problems in the short-term: Main concerning in the shareholders for the gap between actual and budget figures; stressing the team; problems to pay for bonus to high performers because objectives were unrealistic; better employees leaving the company because they are not willing to work in those conditions and they have other better workplaces outside; create cost structure problems because operations make investments to support unrealistic sales volumes; create important cash flow problems because we are using an optimistic scenario.

Making the correct strategic questions about budget

Manager used to ask questions which push people to improve the budget. Common wisdom teach us that budget as objectives should be SMART (Specific, Measurable, Attainable, Relevant, and Timed). But there are leaders who believe that attainable means approximately 10% of probability because they think that this is achievable (there is a probability of 10%) and those “incentive” people to work harder. The reality is for low performers we cannot expect too much, and for high performers they are already working hard. So the result of this approach just used to demotivated high performers. Probably the right strategic questions regarding budget should be to verify the coherency of budget rather than raising objectives too much. For instance in Sales some coherent questions could be:

- What is the average time for closing sales?

- What is the minimum pipeline probability used to incorporate sales pipeline opportunities in the budget?

- What are the additional resources to justify the proposed growth?

- What is the assumption of productivity of new resources in the initial stages (for instance new reps used not to be productive in the initial months)?

- What are the initiatives that support the proposed growth?

Annual budget is an opportunity to learn and questioning our cost structure

There are still organizations that prepare budgets just making the extrapolation of the previous year. Nevertheless, budget is a great opportunity to study the previous year and suggest improvements’ initiatives like travel savings, reducing the number of facilities, etc. There are companies that wait to run under budget to implement improvement initiatives rather than doing proactively.

Questioning company strategy

Sometimes we used to assume that budget must be aligned with strategy, but what about if we have an unrealistic strategy. If there is a misalignment between budget and strategy execution, it is time to discuss if the issue is the budget or it is the strategy.

As we can review, there are many opportunities to improve the budget process and our strategy execution. Materializing those opportunities can make an important difference in the company performance and turnaround process.